The Perks of a 2-1 Rate Buydown: Why Buyers Should Ask and Sellers Should Offer

Interest rates have been the biggest obstacle in today’s housing market. Many qualified buyers hesitate to move forward, not because they can’t afford the home overall, but because the monthly payment feels out of reach with current mortgage rates. This is where a 2-1 rate buydown comes in—a creative financing tool that more buyers should be asking about and more sellers should consider offering.

What is a 2-1 Rate Buydown?

A 2-1 rate buydown is a seller- or lender-funded incentive that temporarily reduces the buyer’s mortgage interest rate:

- Year 1: The rate is 2% lower than the note rate.

- Year 2: The rate is 1% lower.

- Year 3 and beyond: The loan adjusts back to the original fixed rate.

For example, if a buyer locks in a 7% fixed rate, their first-year payments are calculated at 5%, the second year at 6%, and then 7% from year three onward.

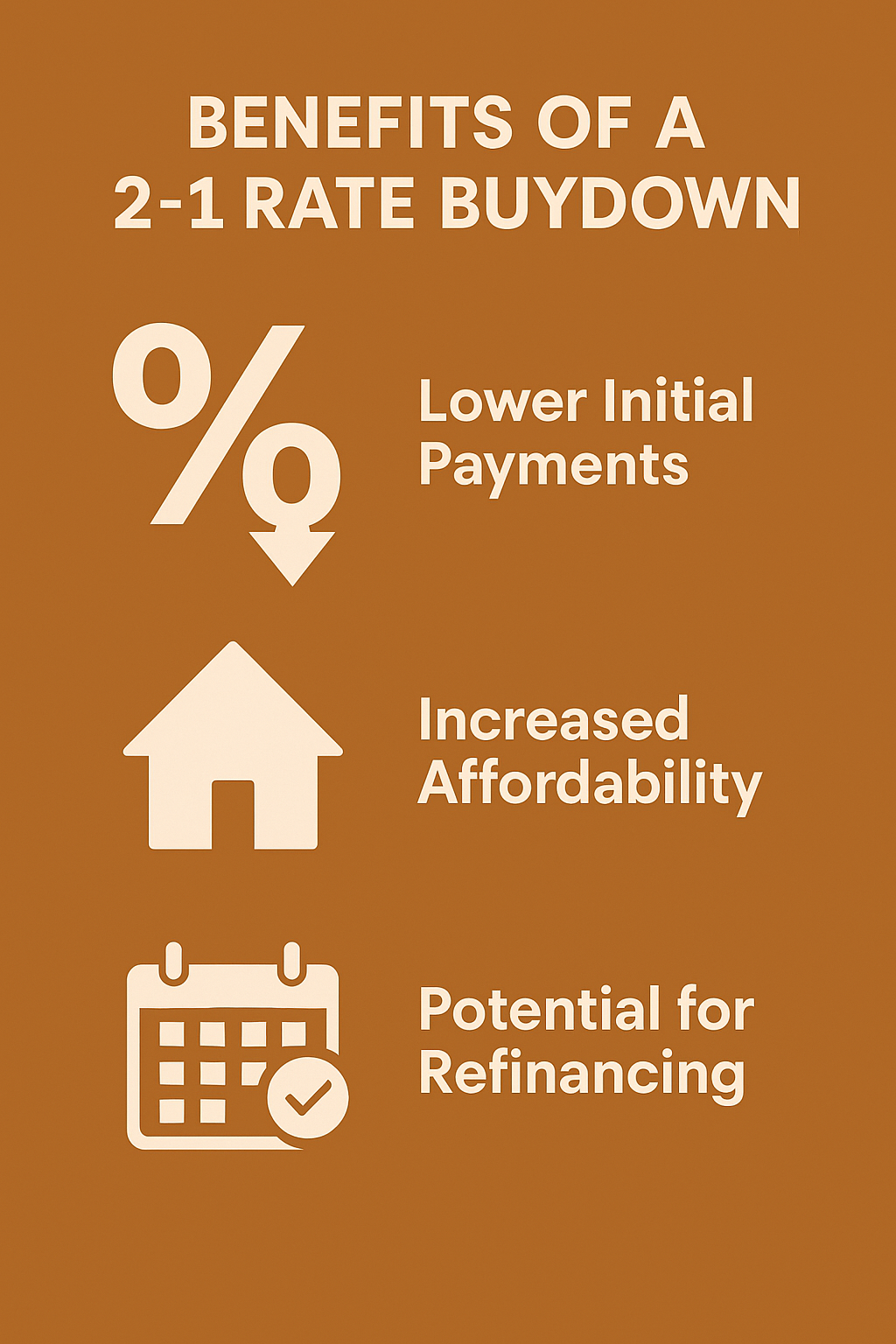

Why Buyers Should Ask for It

- Lower Initial Payments: A buydown can save hundreds of dollars per month in the first two years, giving buyers breathing room as they settle into their new home.

- Better Affordability: Lower payments may help buyers qualify for homes that would otherwise stretch their budget.

- Flexibility for the Future: Many experts anticipate rates could drop within the next few years. If that happens, buyers may refinance before ever paying the full note rate long-term.

Why Sellers Should Consider Offering It

With buyers hesitating due to interest rates, sellers need tools that make their property stand out. Offering a 2-1 buydown can:

- Attract More Buyers: While a $5,000 price reduction may not make much difference to a buyer’s monthly payment, applying those same dollars to a buydown directly lowers their costs.

- Compete in a High-Rate Market: Instead of simply slashing the listing price, sellers can offer a creative incentive that feels more valuable to buyers.

- Faster Sales: Homes marketed with a seller-paid rate buydown often draw more interest, shorten time on market, and reduce the risk of additional price cuts later.

How It Compares to a Price Drop

A $10,000 price cut might only reduce a buyer’s monthly payment by around $50–$70. In contrast, the same $10,000 applied to a 2-1 buydown can reduce their payments by hundreds per month in the first two years. That’s a benefit buyers truly feel, especially in today’s market.

Final Thoughts

The 2-1 rate buydown is a win-win solution. Buyers should ask their agents and lenders if this option is available when making an offer. Sellers should discuss with their listing agent whether offering this incentive makes sense for their property. In a market where interest rates create hesitation, a 2-1 buydown may be the key to bridging the gap between buyers and sellers.

Thinking about buying or selling in Mobile, AL?

Let’s talk about how a 2-1 rate buydown or other creative strategies can help you reach your goals in today’s market.

📞 Call/Text me at [251-272-1827]